In the complex world of finance and investment, understanding the concept of fair value is crucial for making informed decisions. Fair value is a fundamental principle that helps investors, analysts, and financial professionals assess the true worth of assets, securities, and companies. This comprehensive guide will delve into the intricacies of fair value, exploring its definition, importance, calculation methods, and practical applications in the investment landscape.

As we navigate this topic, we’ll examine how fair value influences various aspects of investing, from financial reporting to investment strategies. We’ll also discuss the challenges in determining fair value and how regulatory bodies have shaped its implementation in financial markets. By the end of this article, you’ll have a thorough understanding of fair value and how it can be leveraged to enhance your investment decisions.

Defining Fair Value

What is Fair Value?

Fair value is an estimate of the potential market price of an asset or liability, based on current market conditions and assumptions that market participants would use when pricing the asset or liability. It represents the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

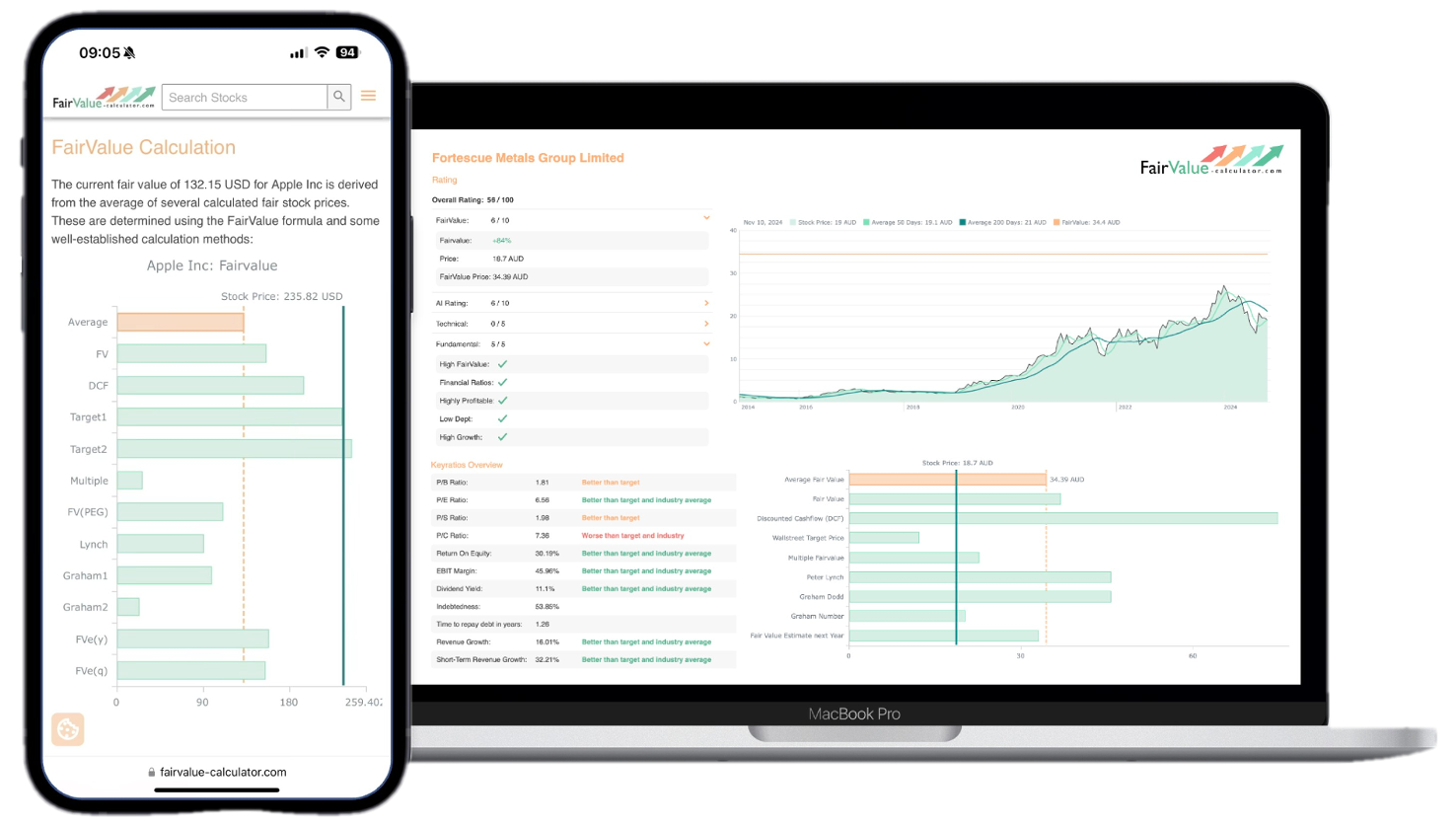

Explore our most popular stock fair value calculators to find opportunities where the market price is lower than the true value.

- Peter Lynch Fair Value – Combines growth with valuation using the PEG ratio. A favorite among growth investors.

- Buffett Intrinsic Value Calculator – Based on Warren Buffett’s long-term DCF approach to determine business value.

- Buffett Fair Value Model – Simplified version of his logic with margin of safety baked in.

- Graham & Dodd Fair Value – Uses conservative earnings-based valuation from classic value investing theory.

- Intrinsic vs. Extrinsic Value – Learn the core difference between what a company’s really worth and what others pay.

- Intrinsic Value Calculator – A general tool to estimate the true value of a stock, based on earnings potential.

- Fama-French Model – For advanced users: Quantifies expected return using size, value and market risk.

- Discount Rate Calculator – Helps estimate the proper rate to use in any DCF-based valuation model.

The concept of fair value is rooted in the idea that the true worth of an asset or liability should reflect current market conditions rather than historical costs or arbitrary valuations. This approach provides a more accurate and relevant picture of an entity’s financial position and performance.

Fair Value vs. Market Value

💡 Discover Powerful Investing Tools

Stop guessing – start investing with confidence. Our Fair Value Stock Calculators help you uncover hidden value in stocks using time-tested methods like Discounted Cash Flow (DCF), Benjamin Graham’s valuation principles, Peter Lynch’s PEG ratio, and our own AI-powered Super Fair Value formula. Designed for clarity, speed, and precision, these tools turn complex valuation models into simple, actionable insights – even for beginners.

Learn More About the Tools →While often used interchangeably, fair value and market value are not always the same:

- Market value refers to the actual price at which an asset is traded in the market.

- Fair value is an estimate of what the market value should be, based on all available information and assumptions about market conditions.

In efficient markets with high liquidity, fair value, and market value tend to converge. However, in less efficient or illiquid markets, there can be significant discrepancies between the two.

The Evolution of Fair Value in Accounting

The concept of fair value has evolved significantly in accounting practices over the past few decades:

- Historical cost accounting: Traditionally, assets were recorded at their original purchase price (historical cost).

- Mark-to-market accounting: This approach values assets based on their current market price.

- Fair value accounting: A more comprehensive approach that considers market conditions, risks, and other factors to estimate the true value of assets and liabilities.

The shift towards fair value accounting has been driven by the need for more relevant and timely financial information in an increasingly complex and fast-paced global economy.

The Importance of Fair Value in Investing

Enhancing Financial Transparency

Fair value provides investors with a more accurate picture of a company’s financial position:

- Asset valuation: It helps investors understand the current worth of a company’s assets, rather than relying on outdated historical costs.

- Liability assessment: Fair value accounting also applies to liabilities, giving a more realistic view of a company’s obligations.

- Performance measurement: By reflecting current market conditions, fair value allows for a better assessment of management’s performance in utilizing company resources.

Facilitating Informed Decision-Making

Understanding fair value empowers investors to make more informed decisions:

- Comparison across companies: Fair value provides a standardized approach, making it easier to compare companies within and across industries.

- Identifying undervalued or overvalued assets: By comparing fair value estimates to market prices, investors can spot potential investment opportunities.

- Risk assessment: Fair value disclosures often include information about the assumptions and methods used, helping investors assess the level of uncertainty in valuations.

Improving Market Efficiency

The widespread adoption of fair value principles contributes to overall market efficiency:

- Price discovery: As more information is incorporated into fair value estimates, it helps markets arrive at more accurate prices for assets and securities.

- Reduced information asymmetry: Fair value disclosures level the playing field between insiders and outside investors, promoting fairer markets.

- Early warning system: Fair value accounting can highlight potential issues in asset values before they become critical, allowing for timely interventions.

Methods of Calculating Fair Value

Market Approach

The market approach relies on observable market data to estimate fair value:

- Comparable transactions: This method looks at recent sales of similar assets to determine fair value.

- Market multiples: Valuation ratios (e.g., price-to-earnings, price-to-book) from comparable companies are used to estimate fair value.

Advantages

- Based on real market data

- Relatively simple to understand and apply

Disadvantages

- This may not apply to unique or illiquid assets

- Can be distorted by market inefficiencies or temporary fluctuations

Income Approach

The income approach estimates fair value based on the expected future cash flows an asset will generate:

- Discounted Cash Flow (DCF) analysis: This method involves projecting future cash flows and discounting them back to present value.

- Capitalization of earnings: This technique uses a single period’s earnings and applies a capitalization rate to estimate fair value.

Advantages

- Considers the asset’s future economic benefits

- Can be applied to a wide range of assets, including those without readily observable market prices

Disadvantages

- Relies heavily on assumptions about future performance

- Can be complex and time-consuming

Cost Approach

The cost approach estimates fair value based on the cost to replace or reproduce an asset:

- Replacement cost: This method considers the cost to replace an asset with a new one of equivalent utility.

- Reproduction cost: This approach looks at the cost to create a replica of the asset.

Advantages

- Useful for valuing specialized assets or those with no active market

- Relatively straightforward to apply

Disadvantages

- May not account for intangible factors that contribute to an asset’s value

- Can overstate value for obsolete assets

Fair Value Hierarchy

The Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) have established a fair value hierarchy to categorize the inputs used in fair value measurements:

Level 1 Inputs

- Definition: Quoted prices in active markets for identical assets or liabilities.

- Examples: Stock prices on major exchanges, and commodity prices on futures markets.

- Reliability: Considered the most reliable and objective measure of fair value.

Level 2 Inputs

- Definition: Observable inputs other than Level 1 prices, such as quoted prices for similar assets, interest rates, yield curves, etc.

- Examples: Bond prices derived from yield curves, and valuations based on comparable company multiples.

- Reliability: Less reliable than Level 1 but still based on observable market data.

Level 3 Inputs

- Definition: Unobservable inputs based on the entity’s assumptions about market participant assumptions.

- Examples: Valuations of private companies, complex derivatives, and illiquid real estate.

- Reliability: Considered the least reliable and most subjective measure of fair value.

Understanding this hierarchy is crucial for investors, as it provides insight into the reliability and potential subjectivity of reported fair values.

Challenges in Determining Fair Value

Market Volatility and Illiquidity

- Rapidly changing market conditions can make it difficult to determine a stable fair value.

- Illiquid markets may not provide enough price information to make accurate fair value estimates.

Complexity of Financial Instruments

- Complex derivatives and structured products often lack observable market prices.

- The intricate nature of these instruments can make modeling their fair value extremely challenging.

Subjectivity and Estimation Uncertainty

- Level 3 fair value measurements rely heavily on management’s assumptions and judgments.

- Different valuation models and assumptions can lead to significantly different fair value estimates.

Procyclicality Concerns

- Fair value accounting can potentially amplify economic cycles by forcing write-downs during market downturns.

- This can lead to a feedback loop where falling asset prices trigger further selling, exacerbating market declines.

Regulatory Framework and Fair Value

FASB and IASB Standards

- ASC 820 (US GAAP) and IFRS 13: These standards provide a framework for measuring fair value and required disclosures.

- Convergence efforts: The FASB and IASB have worked to align their fair value standards, promoting global consistency.

SEC Guidance

- The Securities and Exchange Commission (SEC) has issued guidance on fair value measurements, particularly during periods of market dislocation.

- Enhanced disclosure requirements aim to improve transparency around fair value estimates.

Basel Committee on Banking Supervision

- The Basel Committee has incorporated fair value considerations into its regulatory framework for banks.

- Guidelines address the use of fair value in determining regulatory capital and risk management practices.

Practical Applications of Fair Value for Investors

Financial Statement Analysis

- Understanding fair value adjustments can provide insights into a company’s true financial position.

- Analyzing fair value disclosures can reveal potential risks and uncertainties in valuations.

Valuation Models

- Incorporating fair value concepts into valuation models can lead to more accurate company valuations.

- Adjusting for differences between reported fair values and an investor’s estimates can refine valuation outcomes.

Risk Assessment

- Examining the composition of fair value measurements (Levels 1, 2, 3) can indicate the level of valuation risk in a company’s assets.

- Understanding the sensitivity of fair value estimates to key assumptions can help quantify potential downside risks.

Identifying Investment Opportunities

- Comparing market prices to fair value estimates can help identify potentially undervalued or overvalued securities.

- Analyzing trends in fair value adjustments over time can provide insights into a company’s performance and market positioning.

The Future of Fair Value in Investing

Technological Advancements

- Artificial intelligence and machine learning are being increasingly used to improve fair value estimates.

- Blockchain technology may enhance the transparency and reliability of fair value measurements.

Evolving Regulatory Landscape

- Ongoing debates about the role of fair value accounting in financial stability may lead to further refinements in regulations.

- Increased focus on non-financial factors (e.g., ESG considerations) may influence fair value methodologies.

Market Participant Behavior

- As investors become more sophisticated in understanding fair value, market efficiency may improve.

- The growing importance of intangible assets may challenge traditional fair value measurement approaches.

Understanding fair value is essential for investors navigating today’s complex financial markets. While it provides a more relevant and timely picture of asset and liability values, it also introduces challenges in terms of measurement and interpretation. By grasping the concepts, methods, and applications of fair value, investors can make more informed decisions, better assess risks, and potentially identify lucrative investment opportunities.

As financial markets continue to evolve, the concept of fair value is likely to remain a cornerstone of financial reporting and analysis. Staying informed about developments in fair value practices, regulations, and technologies will be crucial for investors seeking to maintain a competitive edge in the ever-changing investment landscape.

Remember, while fair value provides valuable insights, it should be used in conjunction with other analytical tools and considered within the broader context of a company’s business model, industry dynamics, and macroeconomic factors. By doing so, investors can leverage the power of fair value to enhance their investment strategies and potentially achieve superior long-term returns.